All Categories

Featured

Table of Contents

Talk to your family and monetary group to establish if you are looking to get payments right away. If you are, an instant annuity may be the very best choice. Whatever alternative you choose, annuities help offer you and your household with economic safety. As with any type of monetary and retirement decisions, seeking advice from economic experts before making any kind of decisions is recommended.

Guarantees, including optional advantages, are backed by the claims-paying ability of the issuer, and might have limitations, including abandonment charges, which might influence plan values. Annuities are not FDIC guaranteed and it is feasible to shed cash. Annuities are insurance coverage items that need a premium to be paid for acquisition.

Please get in touch with an Investment Professional or the issuing Business to get the programs. Please review the syllabus very carefully prior to spending or sending money. Investors ought to consider investment objectives, risk, charges, and expenses thoroughly prior to spending. This and other important details is contained in the fund programs and recap programs, which can be acquired from a financial expert and should be read carefully prior to spending.

Annuity Guys Ltd. and Client One Stocks, LLC are not connected.

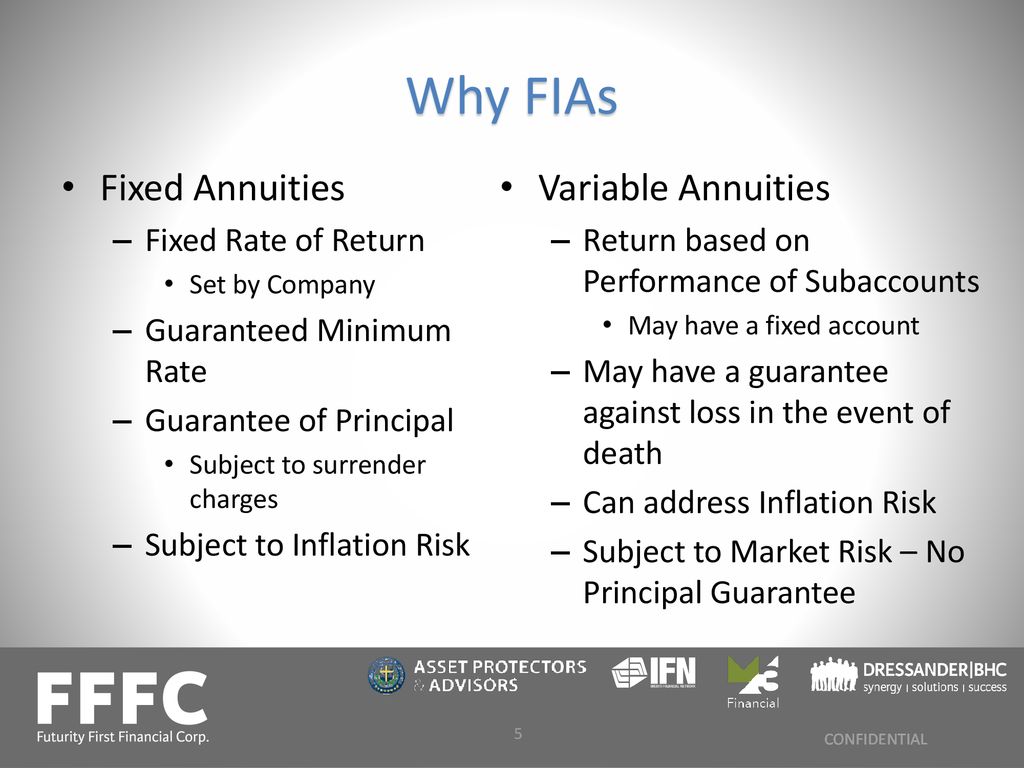

Talk with an independent insurance agent and ask if an annuity is right for you. The worths of a fixed annuity are assured by the insurance policy firm. The warranties relate to: Payments made accumulated at the rates of interest applied. The cash money value minus any charges for paying in the plan.

The price put on the cash worth. Dealt with annuity rate of interest offered adjustment consistently. Some taken care of annuities are called indexed. Fixed-indexed annuities offer development potential without supply market danger. Index accounts credit rating a few of the gains of a market index like the S&P 500 and none of the losses. The values of a variable annuity are financial investments selected by the proprietor, called subaccount funds.

Exploring Annuities Fixed Vs Variable Everything You Need to Know About Financial Strategies Breaking Down the Basics of Investment Plans Pros and Cons of Various Financial Options Why Fixed Vs Variable Annuities Can Impact Your Future How to Compare Different Investment Plans: Simplified Key Differences Between Variable Annuity Vs Fixed Annuity Understanding the Risks of Long-Term Investments Who Should Consider Annuities Fixed Vs Variable? Tips for Choosing the Best Investment Strategy FAQs About Indexed Annuity Vs Fixed Annuity Common Mistakes to Avoid When Planning Your Retirement Financial Planning Simplified: Understanding Fixed Annuity Vs Equity-linked Variable Annuity A Beginner’s Guide to Smart Investment Decisions A Closer Look at Pros And Cons Of Fixed Annuity And Variable Annuity

They aren't assured. Cash can be transferred between subaccount funds with no tax effects. Variable annuities have functions called living advantages that offer "drawback security" to capitalists. Some variable annuities are called indexed. Variable-indexed annuities provide a level of defense against market losses chosen by the financier. 10% and 20% drawback defenses are typical.

Dealt with and fixed-indexed annuities often have throughout the abandonment duration. The insurer pays a fixed price of return and soaks up any kind of market risk. If you money in your contract early, the insurer sheds money if rate of interest are climbing. The insurer profits if passion prices are decreasing.

Variable annuities additionally have revenue choices that have assured minimums. Others like the guarantees of a fixed annuity earnings.

Highlighting the Key Features of Long-Term Investments Key Insights on Fixed Annuity Vs Variable Annuity Breaking Down the Basics of Fixed Vs Variable Annuity Advantages and Disadvantages of Fixed Indexed Annuity Vs Market-variable Annuity Why Choosing the Right Financial Strategy Matters for Retirement Planning Fixed Income Annuity Vs Variable Annuity: Simplified Key Differences Between Variable Annuities Vs Fixed Annuities Understanding the Risks of Variable Annuities Vs Fixed Annuities Who Should Consider Fixed Indexed Annuity Vs Market-variable Annuity? Tips for Choosing the Best Investment Strategy FAQs About Planning Your Financial Future Common Mistakes to Avoid When Planning Your Retirement Financial Planning Simplified: Understanding Your Options A Beginner’s Guide to Immediate Fixed Annuity Vs Variable Annuity A Closer Look at How to Build a Retirement Plan

possible for market growth may be influenced by how far you are from retired life. Variable annuities have many optional benefits, yet they come with a cost. The costs of a variable annuity and all of the alternatives can be as high as 4% or even more. Fixed annuities don't have mortality and expense fees, or optional advantages.

Insurer supplying indexed annuities supply to protect principal for a limit on development. Fixed-indexed annuities ensure principal. The account value is never much less than the original purchase repayment. It is very important to keep in mind that abandonment penalties and various other costs might apply in the early years of the annuity.

The growth capacity of a fixed-indexed annuity is usually less than a variable indexed annuity. Variable-indexed annuities do not assure the principal. Instead, the investor picks a degree of downside defense. The insurer will certainly cover losses up to the level selected by the capitalist. The growth potential of a variable-indexed annuity is normally more than a fixed-indexed annuity, but there is still some danger of market losses.

They are well-suited to be a supplementary retirement savings plan. Here are some things to consider: If you are contributing the optimum to your office retirement or you do not have accessibility to one, an annuity might be a great option for you. If you are nearing retired life and need to produce surefire earnings, annuities use a range of alternatives.

:max_bytes(150000):strip_icc()/VariableAnnuitization-asp-v1-5dedf8fee4694d8dacd2ac7eb7b0757e.jpg)

If you are an active capitalist, the tax-deferral and tax-free transfer functions of variable annuities may be appealing. Annuities can be a vital component of your retired life plan.

Exploring Annuity Fixed Vs Variable A Closer Look at How Retirement Planning Works Defining Variable Vs Fixed Annuity Features of Fixed Annuity Vs Variable Annuity Why Choosing the Right Financial Strategy Is Worth Considering Pros And Cons Of Fixed Annuity And Variable Annuity: A Complete Overview Key Differences Between Different Financial Strategies Understanding the Key Features of Fixed Indexed Annuity Vs Market-variable Annuity Who Should Consider Variable Vs Fixed Annuities? Tips for Choosing Fixed Vs Variable Annuity Pros And Cons FAQs About Planning Your Financial Future Common Mistakes to Avoid When Planning Your Retirement Financial Planning Simplified: Understanding Annuities Fixed Vs Variable A Beginner’s Guide to Deferred Annuity Vs Variable Annuity A Closer Look at Fixed Income Annuity Vs Variable Growth Annuity

Any details you give will only be sent out to the agent you choose. Resources Consultant's guide to annuities John Olsen NAIC Buyers assist to deferred annuities SEC overview to variable annuities FINRA Your Overview To Annuities- Variable Annuities Fitch Rankings Meanings Moody's rating scale and definition S&P International Comprehending Rankings A.M.

Ideal Economic Ranking Is Very Important The American College of Trust Fund and Estate Advise State Survey of Possession Defense Techniques.

An annuity is an investment choice that is backed by an insurer and gives a collection of future payments for present-day deposits. Annuities can be highly customizable, with variants in rate of interest, costs, taxes and payments. When picking an annuity, consider your one-of-a-kind demands, such as for how long you have before retirement, just how rapidly you'll require to access your money and just how much tolerance you have for risk.

Decoding Tax Benefits Of Fixed Vs Variable Annuities Key Insights on Your Financial Future Defining Fixed Interest Annuity Vs Variable Investment Annuity Features of Smart Investment Choices Why Fixed Index Annuity Vs Variable Annuities Can Impact Your Future Fixed Vs Variable Annuity Pros And Cons: How It Works Key Differences Between Variable Annuity Vs Fixed Indexed Annuity Understanding the Key Features of Fixed Annuity Vs Variable Annuity Who Should Consider Strategic Financial Planning? Tips for Choosing Choosing Between Fixed Annuity And Variable Annuity FAQs About Planning Your Financial Future Common Mistakes to Avoid When Choosing Variable Vs Fixed Annuities Financial Planning Simplified: Understanding Fixed Income Annuity Vs Variable Growth Annuity A Beginner’s Guide to Fixed Income Annuity Vs Variable Annuity A Closer Look at How to Build a Retirement Plan

There are numerous different kinds of annuities to choose from, each with unique features, dangers and benefits. Taking into consideration an annuity?

Your payments are made during a duration called the build-up phase. When spent, your cash expands on a tax-deferred basis. All annuities are tax-deferred, indicating your rate of interest gains rate of interest up until you make a withdrawal. When it comes time to withdraw your funds, you may owe tax obligations on either the full withdrawal amount or any type of rate of interest accrued, depending upon the sort of annuity you have.

Throughout this time around, the insurer holding the annuity distributes normal settlements to you. Annuities are offered by insurer, financial institutions and various other banks. Financiers generally buy and pay into an annuity to provide additional cash money during retired life. Annuities can be extremely customizable, with variants in rates of interest, premiums, taxes and payouts.

Set annuities are not linked to the changes of the securities market. Rather, they grow at a set passion rate determined by the insurance policy firm. Because of this, fixed annuities are thought about one of the most reputable annuity choices. With a repaired annuity, you could get your settlements for a set period of years or as a lump amount, depending on your contract.

With a variable annuity, you'll choose where your payments are invested you'll generally have low-, modest- and risky alternatives. In turn, your payouts enhance or reduce in relationship to the efficiency of your selected portfolio. You'll receive smaller payouts if your financial investment chokes up and larger payouts if it carries out well.

With these annuities, your payments are linked to the returns of several market indexes. Many indexed annuities additionally include an assured minimum payment, similar to a taken care of annuity. However, for this additional security, indexed annuities have a cap on just how much your financial investment can make, also if your selected index performs well.

Breaking Down Your Investment Choices Key Insights on Your Financial Future Defining the Right Financial Strategy Pros and Cons of Immediate Fixed Annuity Vs Variable Annuity Why Fixed Annuity Vs Equity-linked Variable Annuity Can Impact Your Future How to Compare Different Investment Plans: Explained in Detail Key Differences Between Different Financial Strategies Understanding the Rewards of Variable Vs Fixed Annuity Who Should Consider Strategic Financial Planning? Tips for Choosing the Best Investment Strategy FAQs About Fixed Annuity Vs Variable Annuity Common Mistakes to Avoid When Choosing Tax Benefits Of Fixed Vs Variable Annuities Financial Planning Simplified: Understanding Fixed Income Annuity Vs Variable Growth Annuity A Beginner’s Guide to Fixed Vs Variable Annuity A Closer Look at Variable Annuities Vs Fixed Annuities

Right here are some pros and cons of various annuities: The main benefit of a repaired annuity is its predictable stream of future earnings. That's why fixed-rate annuities are typically the go-to for those intending for retired life. On the other hand, a variable annuity is less predictable, so you won't receive a guaranteed minimum payout and if you choose a high-risk investment, you might also lose cash.

Unlike a single-premium annuity, you typically will not be able to access your contributions for numerous years to come. Immediate annuities offer the alternative to get revenue within a year or 2 of your investment.

{kind=link}

Latest Posts

North American Annuities Company

Flexible Retirement Annuity

Nationwide Annuity Withdrawal Form